Analysing the Business Environment

Introduction

Banks operate within a larger ecosystem and engage with customers and other businesses. Additionally, banks have an internal environment that they interact with, and both environments require analysis. This article will illustrate the use of business environment analysis techniques, not only for external business analysis but also for examining the internal environment.

External Environment

Two techniques were used to analyse the external environment of Unhappy Bank.

Porter’s Five Forces

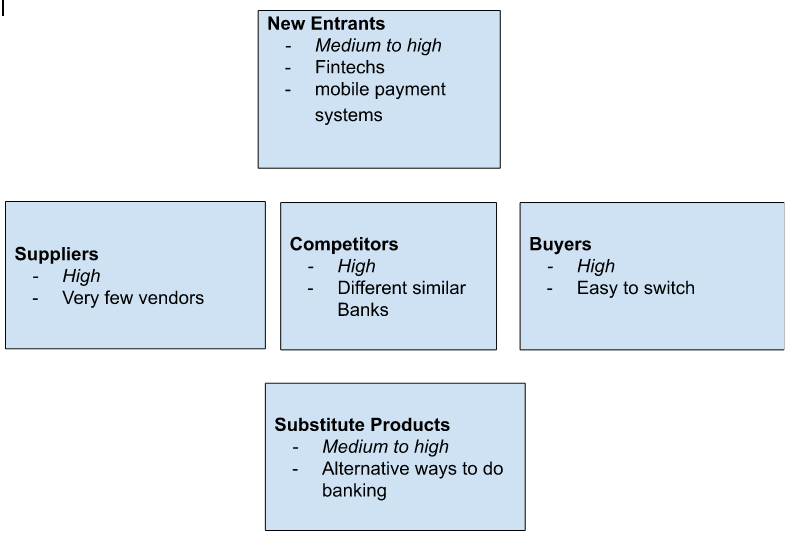

A well known framework developed by Michael Porter in 1979 that helps businesses analyze and evaluate the competitive forces within an industry or market. The five forces are:

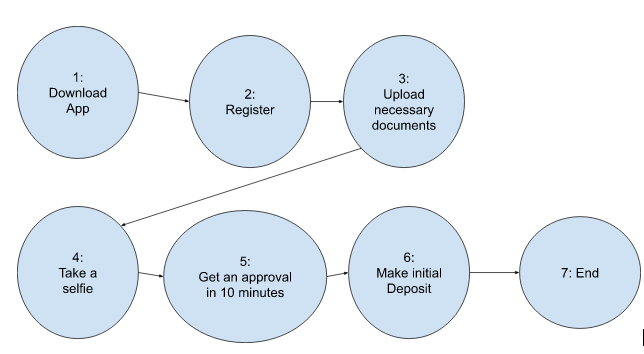

1. Threat of New Entrants: The degree of difficulty for new companies to enter the market. The banking industry has high barriers to entry due to regulatory requirements and high capital requirements, making it difficult for new players to enter the market. However, with the rise of fintech startups, online banking, and mobile payment systems, new entrants can disrupt the industry and offer alternative banking solutions to customers. Unhappy Bank utilized a cumbersome on-boarding process that involved paperwork and in-person visits to a branch, in contrast to well-known fintechs that can on board new customers with ease through mobile apps. As a result, it was evident that the on boarding process required a complete overhaul. The below diagram illustrates a typical 15 minute on-boarding process of a fintech company.

15 Minutes on-boarding process

15 Minutes on-boarding process

2. Bargaining Power of Suppliers: The level of influence that suppliers have on the price and quality of goods and services. Unhappy Bank relied on very specific suppliers such as technology vendors, security providers, and marketing agencies located in the same country. Unhappy Bank soon realised that these suppliers had moderate bargaining power as there were many suppliers in the international market.

3. Bargaining Power of Buyers: The level of influence that buyers have on the price and quality of goods and services. Unhappy Bank Customers had high bargaining power due to the availability of options, ease of switching between banks, and low switching costs. For example in the UK, the Current Account Switch Service makes switching your current account simple and easy.

4. Threat of Substitute Products or Services: the extent to which alternative products or services can satisfy customer needs. Unhappy Bank faced a significant threat from substitute products and services such as mobile payment systems, peer-to-peer lending platforms, and online investment platforms. These substitutes offered similar or alternative services with lower fees.

5. Competitive Rivalry: The level of competition between existing companies in the industry. Unhappy Bank had to compete with many large players and smaller community banks for market share.

By assessing these five forces, Unhappy Bank identified the strengths and weaknesses of their position in the market, anticipate changes and made strategic decisions to improve their competitive advantage.

Unhappy’s Bank Porter’s Five Forces Analysis

Unhappy’s Bank Porter’s Five Forces Analysis

PESTLE

PESTLE analysis is a framework that was used to analyse the external factors that could impact Unhappy Bank. PESTLE stands for Political, Economic, Sociocultural, Technological, Legal, and Environmental.

The below diagram illustrates the PESTLE analysis that was done for Unhappy Bank.

Unhappy’s Bank PESTLE analysis

Unhappy’s Bank PESTLE analysis

Internal Environment

Two techniques can be used to explain why the internal business environment is important, VMOST and resource audit.

VMOST

VMOST analysis helped Unhappy Bank to align their vision, mission, objectives, strategies, and tactics to achieve their long-term goals and objectives.

- Vision: The bank’s vision was to become a leading provider of financial services that meet the diverse needs of its customers. The bank aimed to achieve this by offering innovative products and services, exceptional customer service, and building strong relationships with customers.

- Mission: The bank’s mission was to provide a wide range of financial services that help customers achieve their financial goals. This included offering a range of banking products and services, investment products, and advisory services to help customers make informed decisions.

- Objectives: The bank’s objectives included:

- Increasing market share by expanding its customer base through targeted marketing campaigns and developing new products and services.

- Improving customer satisfaction by offering exceptional customer service, personalized financial advice, and convenient banking solutions.

- Enhancing operational efficiency by adopting new technologies, streamlining processes, and reducing costs.

- Improving profitability by increasing revenue and reducing costs through effective risk management, optimizing capital allocation, and developing new revenue streams.

4. Strategy: The bank’s strategy was to differentiate itself from competitors by offering innovative products and services that cater to the evolving needs of its customers. This included investing in new technologies, such as online and mobile banking, to improve the customer experience, and expanding its product and service offerings to meet the changing demands of customers.

5. Tactics: The bank’s tactics included:

- Developing and launching new products and services that meet the evolving needs of customers.

- Investing in new technologies to improve operational efficiency and enhance the customer experience.

- Expanding its geographic reach by opening new branches and offering online and mobile banking services.

- Enhancing its marketing and promotional activities to increase brand awareness and attract new customers.

- Providing personalized financial advice and solutions to customers to help them achieve their financial goals.

Resource Audit

Resource audit was the second technique that used to analyse the internal environment of a Unhappy Bank. It involved identifying and evaluating the resources, capabilities, and competencies that the bank possessed. It involved the following:

- Identify the bank’s key resources: This included physical assets such as branches, equipment, and IT infrastructure, as well as intangible assets such as brand reputation, intellectual property, and customer relationships.

- Assess the bank’s financial resources: This included the bank’s financial position, liquidity, and capital adequacy.

- Evaluate the bank’s human resources: This included the skills, knowledge, and expertise of the bank’s employees. Unhappy Bank needed to ensure that they had the right people with the right skills to deliver their services effectively.

- Analyse the bank’s technological resources: This included the bank’s IT systems, software, and other technological resources.

- Evaluate the bank’s organisational resources: This included the bank’s structure, culture, and processes. Organisational resources are critical for a bank’s ability to manage risk, make decisions, and execute its strategy effectively.

- Assess the bank’s operational resources: This included the bank’s operational processes, procedures, and systems. Operational resources are critical for a bank’s ability to deliver its services efficiently and effectively.

By conducting a resource audit, Unhappy Bank could identify its strengths and weaknesses and make informed decisions about its strategy and operations.

0 Comments

No comments yet. Be the first to start the conversation!

Leave a Response